For beginners as well as veterans in IRA investing, here are a few important things to consider. Newbie investors obviously need education in fundamental matters while long-time investors can always benefit from new ways to enhance their investment strategy.

So, how do you maximize returns from your IRA?

Choose what fits your goals: Traditional or. Roth

Should you go for traditional or for Roth IRA? While your traditional IRA contributions can be classified as tax-deductible, Roths use after-tax money; however, they provide tax-free withdrawals when you reach retirement age. To know more about either type of IRA, visit informative investment websites. Here are a few valuable tips on which to choose:

When you should choose a traditional IRA:

· If you are within a higher tax bracket now, in contrast to your expected level when you reach retirement

· If a tax break now is more preferable to you than tax savings when you retire

· If you have no retirement plan sponsored by your employer because your income is too large to qualify you to directly contribute to a Roth IRA

When you should choose a Roth IRA:

· If you want to stay in your present tax rate

· If you want to diversify your retirement assets, aside from your pre-tax account such as a 401(k)

· If you expect to use the money when you retire and would choose rather to keep it in that account to allow it to grow as long as you want (A Roth IRA will not demand a minimum distribution from a specific age.)

· If you want all your money safely parked somewhere (You can withdraw your original contribution amounts in a Roth IRA at any time.)

Take full advantage of the tax benefits

To maximize returns from your IRA, choose the most appropriate types of stocks. Whatever stock whose value grows in time will provide higher gains for you in an IRA compared to a taxable brokerage account. Nevertheless, dividend-growth stocks will optimize the entire compounding capacity of investing in IRA; hence, you must utilize your IRA through buying individual stocks.

As an example, with two stocks often favored in many portfolios, such as Berkshire Hathaway and Apple, one can assign one in a traditional IRA and hold the other in a taxable brokerage account. Invest $5,000 in each one of these two accounts.

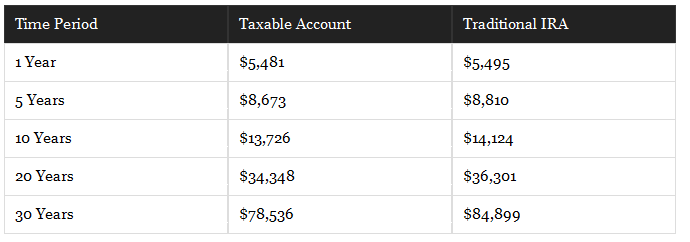

As of today, Apple pays a 1.9% yield in dividends, generating $95 from your $5,000 investment for a year. You will be charged a 15% tax in a taxable brokerage account, effectively giving you about $81 return. However, in a traditional IRA, you get a tax-free deal. Remember: You can now reinvest the entire $95 in more shares, whereas you have less to put back in a taxable account to work with. Although $14 is not that much, the compounding power of money works more in the former than in the latter, especially in the long-term.

To illustrate more clearly, under a 1.9% dividend yield for Apple and a stock gain of 8% annually, you will observe the difference in the gains of an initial investment of $5,000 over time:

Your returns are more obviously higher over a longer period of time than otherwise, as seen in the difference above after 30 years. A $6,400 advantage, more or less, in a traditional IRA is definitely more preferable.

A $5,000 investment in Berkshire Hathaway, in comparison, would only take advantage from an initial tax deduction on your IRA contribution. As Berkshire has no dividend-yield payments, your investment in both kinds of accounts will grow by a fixed amount over time.

The young should invest aggressively now

Allocating too little money or not investing at all could be the worst mistake anyone can make in IRA investing, especially among young investors.

It is natural for millennials to be wary of investing in stocks, considering the early-2000s’ tech crash and the more recent Great Recession, and since many of these millennial investors had parents who lost their investments in the market.

You can use an accepted rule of thumb to determine the percentage of stocks to be included in your portfolio by deducting your age from 110. For instance, if you are 40, around 70% of your money invested must be in stocks. Using this principle will allow your portfolio to become more conservative as you near the retirement age. It is likewise worthwhile to note that ETFs and stock-based mutual funds can serve as good alternative investments if individual stocks do not appeal that much to you.

Just remember that stock investments will always involve volatility. Hence, in any particular year, a 10% drop in the stock market should be expected. Nevertheless, on the long-term, stocks will provide better gains compared to any other types of assets.

Lastly, most of all your investment money will never acquire greater growth opportunity in the long-term than they do in the present, no matter what happens to the market this week or this year. At 25, according to a conservative average of 7% annual growth rate over many years, one only has to invest $5,000 each year ($417 every month) to become a millionaire-retiree at 65. However, at 35, you need to set aside $15,800 each year, or $1,318 monthly, to reach the same level of wealth at 65.

In short, invest as much as you can and as early as you can since time is your most valuable asset, aside from your dollars.